Published on Thursday, April 19, 2018 | Modified on Wednesday, June 5, 2019

")

| Strategy Level | Beginners |

| Instruments Traded | Call + Put |

| Number of Positions | 2 |

| Market View | Neutral |

| Risk Profile | Limited |

| Reward Profile | Unlimited |

| Breakeven Point | two break-even points |

The Long Strangle (or Buy Strangle or Option Strangle) is a neutral strategy wherein Slightly OTM Put Options and Slightly OTM Call are bought simultaneously with same underlying asset and expiry date.

This strategy can be used when the trader expects that the underlying stock will experience significant volatility in the near term.

It is a limited risk and unlimited reward strategy. The maximum loss is the net premium paid while maximum profit is achieved when the underlying moves either significantly upwards or downwards at expiration.

The usual Long Strangle Strategy looks like as below for NIFTY current index value at 10400 (NIFTY Spot Price):

| Orders | NIFTY Strike Price |

|---|---|

| Buy 1 Slightly OTM Put | NIFTY18APR10200PE |

| Buy 1 Slightly OTM Call | NIFTY18APR10600CE |

Suppose Nifty is currently at 10400 and due to some upcoming events you expect the price to move sharply but are unsure about the direction. In such a scenario, you can execute long strangle strategy by buying Nifty Put at 10200 and buying Nifty Call at 10600. The net premium paid will be your maximum loss while the profit will depend on how high or low the index moves.

A Long Strangle is meant for special scenarios where you foresee a lot of volatility in the market due to election results, budget, policy change, annual result announcements etc.

Let's take a simple example of a stock trading at Rs 40 (spot price) in June. The option contracts for this stock are available at the premium of:

Lot size: 100 shares in 1 lot

Net Debit: Rs 100 + Rs 100 = Rs 200

Now let's discuss the possible scenarios:

Scenario 1: Stock price remains unchanged at Rs 40

In this situation,

The total loss of Rs 200 is also the maximum loss in this strategy.

Scenario 2: Stock price goes above Rs 50

In this situation,

Scenario 3: Stock price goes down to Rs 30

In this situation,

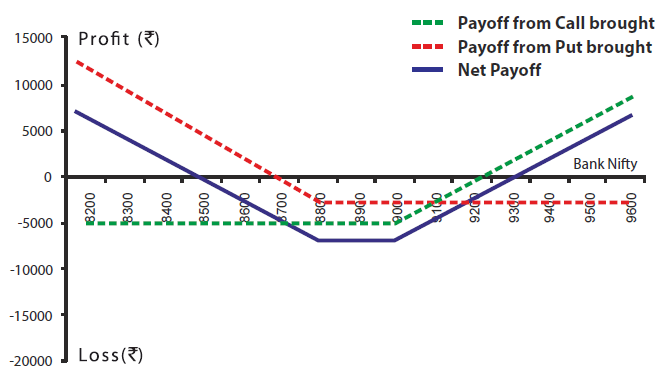

| Bank Nifty Spot Price | 8900 |

| Bank Nifty Lot Size | 25 |

| Strike Price(Rs ) | Premium(Rs ) | Total Premium Paid(Rs ) (Premium * lot size 25) | |

|---|---|---|---|

| Buy 1 OTM Call | 9000 | 200 | 5000 |

| Buy 1 OTM Put | 8800 | 100 | 2500 |

| Net Premium (200+100) | 300 | 7500 | |

| Upper Breakeven(Rs ) | Strike price of Call + Net Premium (9000 + 300) | 9300 |

| Lower Breakeven(Rs ) | Strike price of put - Net Premium (8800 - 300) | 8500 |

| Maximum Possible Loss (Rs ) | Net Premium Paid | 7500 |

| Maximum Possible Profit (Rs ) | Unlimited |

| On Expiry Bank NIFTY closes at | Net Payoff from 1 OTM Call bought (Rs ) @9000 | Net Payoff from 1 OTM Put Bought (Rs ) @8800 | Net Payoff (Rs ) |

|---|---|---|---|

| 8000 | -5000 | 17500 | 12500 |

| 8300 | -5000 | 10000 | 5000 |

| 8500 | -5000 | 5000 | 0 |

| 9000 | -5000 | -2500 | -7500 |

| 9300 | 2500 | -2500 | 0 |

| 9500 | 7500 | -2500 | 5000 |

| 9800 | 15000 | -2500 | 12500 |

When you are unsure of the direction of the underlying but expecting high volatility in it.

Suppose Nifty is currently at 10400 and you expect the price to move sharply but are unsure about the direction. In such a scenario, you can execute long strangle strategy by buying Nifty at 10600 and at 10800. The net premium paid will be your maximum loss while the profit will depend on how high or low the index moves.

two break-even points

A Options Strangle strategy has two break-even points.

Lower Breakeven Point = Strike Price of Put - Net Premium

Upper Breakeven Point = Strike Price of Call + Net Premium

Max Loss = Net Premium Paid

The maximum loss is limited to the net premium paid in the long strangle strategy. It occurs when the price of the underlying is trading between the strike price of Options.

Maximum profit is achieved when the underlying moves significantly up and down at expiration.

Profit = Price of Underlying - Strike Price of Long Call - Net Premium Paid

Or

Profit = Strike Price of Long Put - Price of Underlying - Net Premium Paid

One Option exercised

Both Option not exercised

The strategy requires significant price movements in the underlying to gain profits.