Published on Wednesday, April 18, 2018 | Modified on Wednesday, June 5, 2019

| Strategy Level | Beginners |

| Instruments Traded | Call |

| Number of Positions | 2 |

| Market View | Bearish |

| Risk Profile | Limited |

| Reward Profile | Limited |

| Breakeven Point | Strike Price of Short Call + Net Premium Received |

A Bear Call Spread strategy involves buying a Call Option while simultaneously selling a Call Option of lower strike price on same underlying asset and expiry date. You receive a premium for selling a Call Option and pay a premium for buying a Call Option. So your cost of investment is much lower. The strategy is less risky with the reward limited to the difference in premium received and paid.

This strategy is used when the trader believes that the price of underlying asset will go down moderately. This strategy is also known as the bear call credit spread as a net credit is received upon entering the trade.

The risk and reward both are limited in the strategy.

The bear call spread strategy looks like as below for NIFTY which is currently traded at Rs 10400 (NIFTY Spot Price):

| Orders | NIFTY Strike Price |

|---|---|

| Buy 1 OTM Call | NIFTY18APR10600CE |

| Sell 1 ITM Call | NIFTY18APR10200CE |

Suppose NIFTY shares are trading at 10400. If we are expecting the price of NIFTY to go down in near future, we sell 1 ITM NIFTY Call and buy 1 OTM NIFTY Call.

The trader receives a higher premium for selling a Call while paying the lower premium for buying a Call. If the NIFTY goes down, trader keeps the net premium received which is also the maximum profit.

If the price of Nifty rises, your loss will be limited to the difference between two strike prices minus the net premium received at the time of entering into the strategy.

The bear call spread options strategy is used when you are bearish in market view. The strategy minimizes your risk in the event of prime movements going against your expectations.

Let's take a simple example of a stock trading at Rs 37 (spot price) in June. The option contracts for this stock are available at the premium of:

Lot size: 100 shares in 1 lot

Net Credit: Rs 100 + Rs 300 = Rs 200

Now let's discuss the possible scenarios:

Scenario 1: Stock price remains unchanged at Rs 37

The total profit of Rs 200 is also the maximum profit in this strategy. This is the amount you paid as premium at the time you enter in the trade.

Scenario 2: Stock price goes up to Rs 42

In this scenario, we lost total Rs 300 which is also the maximum loss in this strategy.

Scenario 3: Stock price goes down to Rs 30

Same as scenario 1:

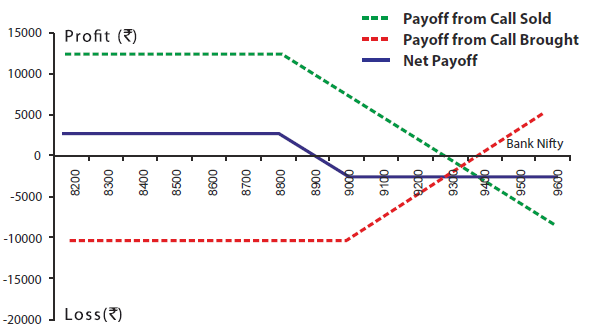

| Bank Nifty Spot Price | 8900 |

| Bank Nifty Lot Size | 25 |

| Strike Price(Rs ) | Premium(Rs ) | Total Premium Paid(Rs ) (Premium * lot size 25) | |

|---|---|---|---|

| Buy 1 OTM Call | 9000 | 400 | 10000 |

| Sell 1 ITM Call | 8800 | 500 | 12500 |

| Net Premium (500-400) | 100 | 2500 | |

| Breakeven(Rs ) | Strike price of the Ssort Call + Net Premium (8800 + 100) | 8900 |

| Maximum Possible Loss (Rs ) | (Strike Price of Long Call - Strike Price of Short Call - Net Premium Received) * Lot Size (9000-8800-100)*25 | 2500 |

| Maximum Possible Profit (Rs ) | Net Premium Received * Lot Size (100)*25 | 2500 |

| On Expiry Bank NIFTY closes at | Net Payoff from 1 ITM Call Sold (Rs ) @8800 | Net Payoff from 1 OTM Call Brought (Rs ) @9000 | Net Payoff (Rs ) |

|---|---|---|---|

| 8500 | 12500 | -10000 | 2500 |

| 8700 | 12500 | -10000 | 2500 |

| 8900 | 10000 | -10000 | 0 |

| 9100 | 5000 | -7500 | -2500 |

| 9300 | 0 | -2500 | -2500 |

When you are expecting the price of the underlying to moderately go down.

Let's assume you're Bearish on Nifty and are expecting mild drop in the price. You can deploy Bear Call strategy by selling a Call Option with lower strike and buying a Call Option with higher strike. You will receive a higher premium for selling a Call while pay lower premium for buying a Call. The net premium will be your profit. If the price of Nifty rises, your loss will be limited to difference between two strike prices minus net premium.

Strike Price of Short Call + Net Premium Received

The break even point is achieved when the price of the underlying is equal to strike price of the short Call plus net premium received.

The maximum loss occurs when the price of the underlying moves above the strike price of long Call.

Maximum Loss = Long Call Strike Price - Short Call Strike Price - Net Premium Received

The maximum profit the net premium received. It occurs when the price of the underlying is greater than strike price of short Call Option.

Max Profit = Net Premium Received - Commissions Paid

Underlying goes down and both options not exercised

Underlying goes up and both options exercised

It allows you to profit in a flat market scenario when you're expecting the underlying to mildly drop, be range bound or marginally rise.

Limited profit potential.