jump in GMP got me interested to dig deeper. here is my analysis. i dont think this one worth the risk to buy.

#Owais #SME #

• Activity:

○ The company is engaged in the manufacturing of the following products;

1. Manganese Oxide (MNO), 2. MC Ferro Manganese, 3. Manufacturing of Wood Charcoal, 4. Processing of Minerals such as Ferro Alloy, Quartz and Manganese Ore.

• Manganese Oxide is used in fertilizer industry; Manganese Ore is used in manufacturing of Ferro Manganese, Silico Manganese, Manganese Oxide, Batteries and other Ferro products. Processed Quartz is being used hotel industry, Ferro Alloys industry, tiles & ceramic industry, glass industry and industry of interiors & furniture

• Market & Customers

○ major products are been supplied to the state of Madhya Pradesh, Maharashtra and Gujrat

○ Our top 10 customers accounted for approximately 95.99% of our revenue from operations in period ended on December 31, 2023

○ As of December 31 2023, our Company’s Order Book was ₹ 16.72 Cr

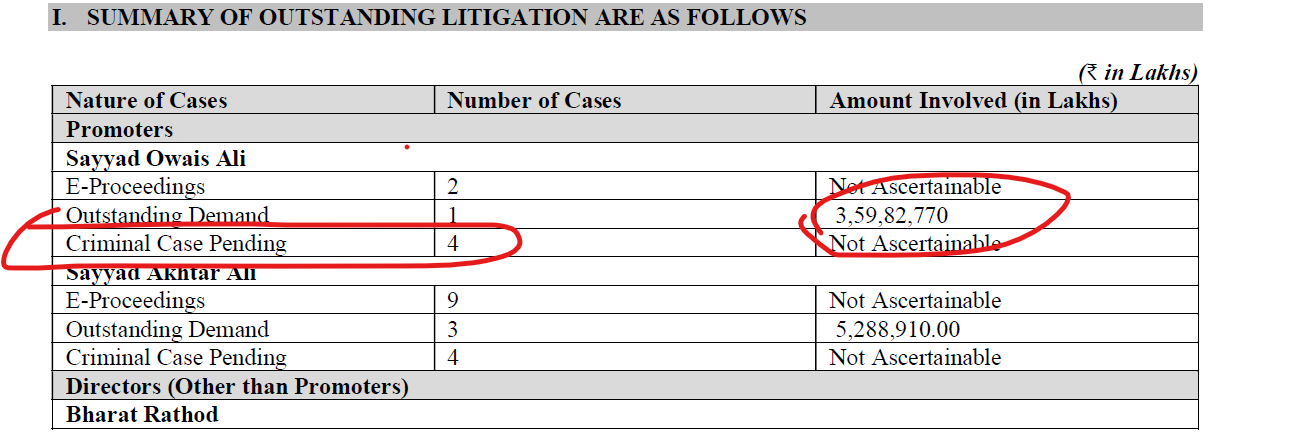

Promoters

• Mr. Saiyyed Owais Ali, Mr. Saiyyed Murtuza Ali and Mr. Sayyad Akhtar Ali.

• 4 crs+ of litigation + 4 criminal cases

• Bad things

○ Cr Issue expenses

○ No EPFO entry found for Owais Metals but for Owais Ali Overseas - 11 Emp

○ Negative operative cashflow

○ 29 Cr trade recieveables against Rev

○ PE of 11 if we assume annualized EPS based on Dec 23 data, with GMP of 140 rs PE goes to ~30 and with a poor order book of 16.72 cr there is no upside upon listing

○ IMFA as a competitor look far more attractive compared to Owais

○ One of the key customer is their own firm SMO Ferro Alloys

○ Sector is of commodity one with none of the customer a listed entity

○ Cap utilization of existing facility seems enough to handle order book so not able to under IPO proceeds towards new facility

• Good things

○ Promoter seems well connected and rich

○ Margin in Dec 31 seems decent if it can be sustained

RHP

RHP