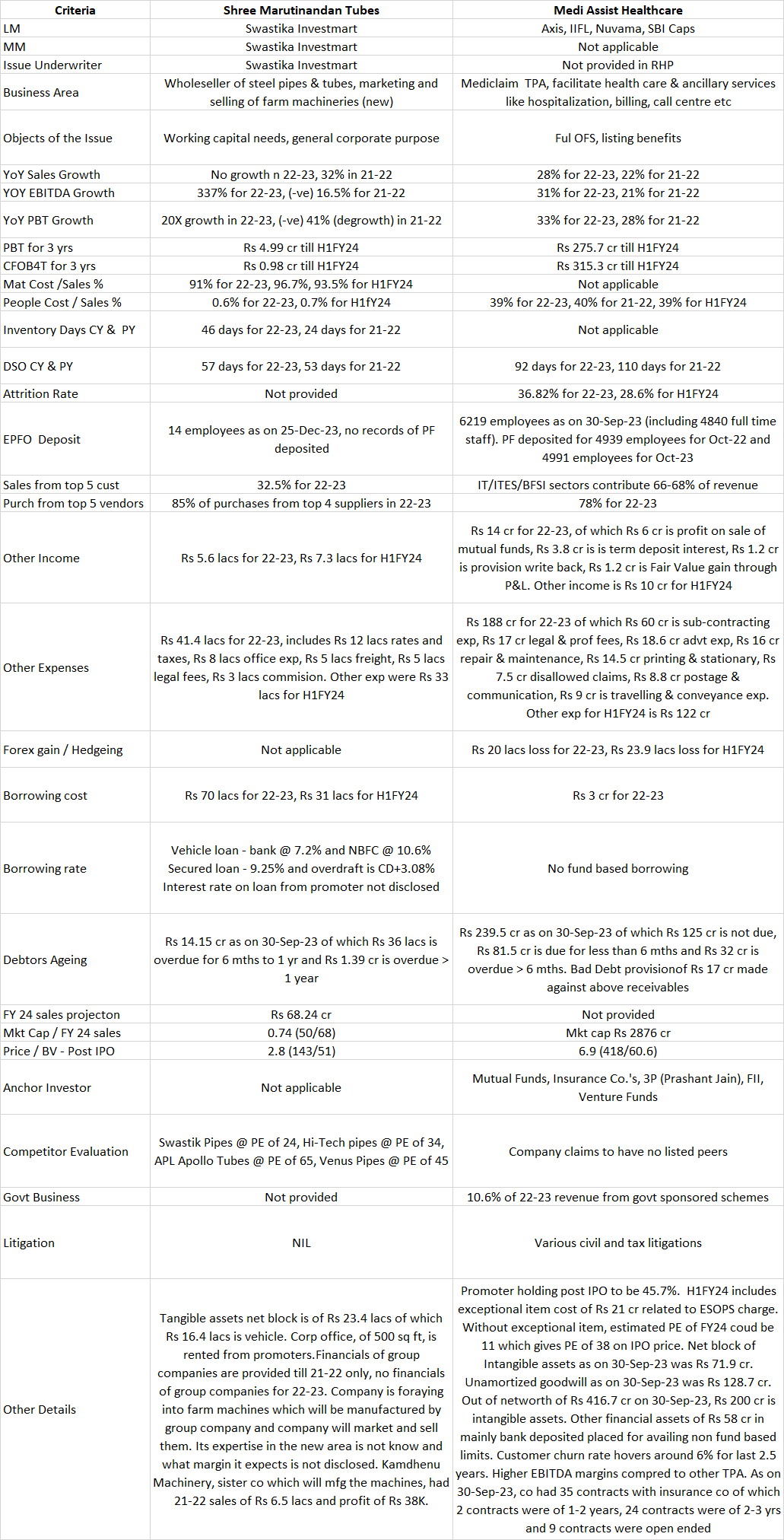

@Sanchit Jain @Aaashish Because of the overlap with 4 other IPOs, I've only kept a very small allocation for this (1 application of 10 lots)

My basic understanding is that

1) In this sector, there is not much manufacturing value add / margin. Even if you look at peers who manufacture, cost of raw material is 90-95% of sales, while manufacturing cost is ~2-3%.

2) Marutinandan's primary contract manufacturer is a group company (Kamdhenu) with the same promoter. That ensures interests are aligned, and margins appear to be shared with Marutinandan.

Raw financials seem alright (very strong for a trading biz - likely because of point 2 above), so I'm viewing this as a trading++ biz with control of manufacturing within the family. But it's still risky compared to say MCPL which was a very easy allotment and great fundamentals, so not going FF, especially with other options available

RHP

RHP