Review By on September 13, 2023

• YOL is India's largest corporate travel service provider enjoying third largest status on the basis of its gross booking and operating revenues for FY23.

• After reporting losses for FY21 and FY22, it has turned the corner in FY23.

• Based on FY23 financial performance the issue is exorbitantly priced.

• The company has posted the highest attrition rates in recent years, which raises concern.

• There is no harm in skipping this pricey bet.

PREFACE:

The company made a pre-IPO placement of 2627697 shares at a price of Rs. 236 per share amounting to Rs. 62.01 cr. in the month of December 2022, and has reduced its fresh equity issue portion of the IPO to that extent. Though the IPO is in the month of September 2023, the offer document has covered financial data only up to March 31, 2023.

ABOUT COMPANY:

Yatra Online Ltd. (YOL) is an online travel agency which spans the entire value chain of travel and hospitality covering B2C and B2B segments. It is India's largest corporate travel services provider in terms of the number of corporate clients and the third-largest online travel company in India among key OTA players in terms of gross booking revenue and operating revenue, for Fiscal Year 2023. (Source: CRISIL Report).

It has the largest number of hotel and accommodation tie-ups amongst key domestic OTA players with over 2,105,600 tie-ups, as of March 31, 2023 (Source: CRISIL Report). Given the size and growth dynamics of the Indian travel market, YOL has strategically focused both on the corporate and consumer markets. It is the leading corporate travel service provider in India with 813 large corporate customers and over 49,800 registered SME customers and the third largest consumer online travel company (OTC) in the country in terms of gross booking revenue for Fiscal 2023 (Source: CRISIL Report).

YOL's go-to-market strategy spans the entire value chain of travel and hospitality covering B2C (business to consumer) and B2B (business to business which includes business to enterprise and business to agents), and this combination enables it to target India's most frequent and high spending travellers, namely, educated urban consumers, in a cost-effective manner. Over 800 large corporate customers of the Company employ over 7.00 million people who along with their families form a large part of the consuming upper middle class of India. In addition, YOL's travel agent network provides additional scale to its business by leveraging an integrated technology platform in order to aggregate consumer demand from over 29,800 travel agents in above 1,000 cities across India as of March 31, 2023. The company is also providing customers with various offerings via its multiple mobile applications. For the fiscal 2023, it provided offerings for over two million hotels globally. As of March 31, 2023, it had 1086 employees on its payroll. The company witnessed a high attrition rate of 58.92% (FY21), 48.37% (FY22), and 60.92% (FY23), which raises concern. Due to the seasonality of its business, its business differs from Quarter-to-Quarter basis.

ISSUE DETAILS/CAPITAL HISTORY:

The company is coming out with its maiden combo IPO of fresh equity shares worth Rs. 602 cr. (approx. 42394380 shares at the upper cap), and an Offer for Sale (OFS) of 12183099 shares (worth Rs. 173.00 cr. at the upper cap). The company has announced a price band of Rs. 135 - Rs. 142 per share of Re. 1 each, and thus the overall size of the issue at the upper cap will be for 54577479 shares worth Rs. 775.00 cr. The issue opens for subscription on September 15, 2023, and will close on September 20, 2023. The minimum application to be made is for 105 shares and in multiples thereon, thereafter. Post allotment, shares will be listed on BSE and NSE. The issue constitutes 34.78% of the post-IPO paid-up capital of the company.

From the net proceeds of the fresh equity issue, it will utilize Rs. 150.00 cr. for strategic investments/acquisitions and inorganic growth, Rs. 392.00 cr. for investment in customer acquisition and retention, technology, and organic growth initiatives, and the rest for general corporate purposes.

The company has allocated not less than 75% for QIBs, not more than 15% for HNIs, and not more than 10% for Retail investors.

SBI Capital Markets Ltd., Dam Capital Advisors Ltd., and IIFL Securities Ltd. are the three joint Book Running Lead Managers (BRLMs) and Link Intime India Pvt. Ltd. is the registrar of the issue.

Having issued initial equity capital at par value, the company issued further equity shares in the price range of Rs. 30.04 - Rs. 306.20 (based on FV of Re. 1) between March 2008 and December 2022. The average cost of acquisition of shares by the promoters/selling stakeholders is Rs. 138.92, Rs. 180.77, and Rs. 185.52 per share. Reliance Group's Reliance Retail and Network 18 has a small stake in this company, and this may be a noteworthy point.

Post-IPO, YOL's current paid-up equity capital of Rs. 11.45 cr. will stand enhanced to Rs. 15.69 cr. At the upper price band of the IPO, the company is looking for a market cap of Rs. 2228.21 cr.

FINANCIAL PERFORMANCE:

On the financial performance front, for the last three fiscals, YOL has (on a consolidated basis) posted a total income/net profit - (loss) of Rs. 143.62 cr. / Rs. - (118.86) cr. (FY21), Rs. 218.81 cr. / Rs. - (30.79) cr. (FY22), and Rs. 397.47 cr. / Rs. 7.63 cr. (FY23). Thus it has turned the corner from FY23. Thanks to security premiums collected that helped the company to post positive NAV.

For the last three fiscals, YOL has reported an average EPS of Rs. - (2.42) and an average RoNW of - (23.96) %. The issue is priced at a P/BV of 9.44 based on its NAV of Rs. 15.04 as of March 31, 2023, and at a P/BV of 2.89 based on post-IPO NAV of Rs. 49.17 per share (at the upper cap).

If we attribute FY23 earnings to the post-IPO fully diluted paid-up equity capital of the company, then the asking price is at a P/E of 289.80. Thus the issue is exorbitantly priced.

For the last three fiscals, the company has reported PAT margins of - (94.75) % (FY21), - (15.54) % (FY22), and 2.01% (FY23). Its margins on Air Ticketing and Hotels and Packages have marked decline while Other Services has marginally improved.

DIVIDEND POLICY:

The company has not declared any dividends for the reported periods of the offer document. It has adopted a prudent dividend policy in March 2022, based on its financial performance and future prospects.

COMPARISON WITH LISTED PEERS:

As per the offer document, the company has shown Easy Trip Planners as their listed peer. It is trading at a P/E of 48.58 (as of September 13, 2023). However, they are not truly comparable on an apple-to-apple basis.

MERCHANT BANKER'S TRACK RECORD:

The three BRLMs associated with the offer have handled 65 public issues in the past three years, out of which 25 issues closed below the IPO price on the listing date.

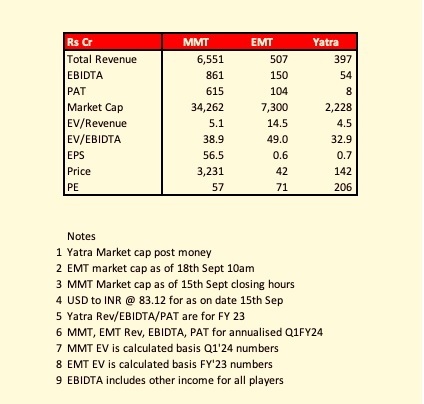

Date: 18th Sept 2023

Automation of back-end processes and increased adoption of our Self Booking Tool (SBT) by our B2B customers has made certain manual processes redundant leading to commensurate rationalization of workforce. These two factors combined would have contribution to a majority of the attrition. It should be considered as non-regrettable attrition.

It is important to compare the valuation through multiple metrics in order to arrive at the right benchmarking. EV/Revenue and EV/EBIDTA are important metrics for high growth markets. Our IPO is priced at a 13% -15% discount to MMT and 33-70% discount to EMT on both these metrics.

Review By on September 13, 2023

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Dilip Davda

SEBI Registered Research Analyst – Mumbai

Registration No.: INH000003127 (Perpetual)

Email: dilip_davda@rediffmail.com

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.

The initial public offer (IPO) of Yatra Online Ltd. offers an early investment opportunity in Yatra Online Ltd.. A stock market investor can buy Yatra Online IPO shares by applying in IPO before Yatra Online Ltd. shares get listed at the stock exchanges. An investor could invest in Yatra Online IPO for short term listing gain or a long term.

Read the Yatra Online IPO recommendations by the leading analyst and leading stock brokers.

Yatra Online IPO offers an opportunity to buy IPO shares before they get listed at the stock exchanges. Read the Yatra Online IPO Notes, Analysis and Recommendations by leading stock brokerage firms and experts mentioned in the above answer to "How is Yatra Online IPO?"

Our recommendation for Yatra Online IPO is to avoid.

As per the analysis by our lead analyst Mr. Dilip Davda, we suggest you to avoid the Yatra Online IPO.

The Yatra Online IPO allotment status will be available on or around September 25, 2023. The allotted shares will be credited in demat account by September 27, 2023. Visit Yatra Online IPO allotment status to check.