FREE Equity Delivery and MF

Flat ₹20/trade Intra-day/F&O

FREE Equity Delivery and MF

Flat ₹20/trade Intra-day/F&O

|

|

NCD IPO is the issuance of debt securities by companies to the general public. Unlike Equity IPO, a company can issue NCD IPO multiple times if it needs funds.

Content:

In recent times, NCD IPO has become very popular among retail investors as it offers investors an opportunity to earn a fixed income at regular intervals. The NCD IPO opens up access to the Indian corporate debt market. Compared to equities, NCDs are considered a safer investment option as investors are guaranteed a fixed return.

NCD IPO is the issuance of debt securities by companies to the general public. Unlike Equity IPO, a company can issue NCD IPO multiple times if it needs funds. For example, in 2023, Muthoot Fincorp issued NCD IPO 4 times in a year. Each NCD issue has a different series of tenor and interest rates depending on the interest rates prevailing at the time of issue.

A company can either file a separate prospectus for each issue or a shelf prospectus that allows it to offer securities over a period of time without filing a new prospectus. In these cases, the company must prepare a tranche prospectus containing the details of each tranche. In this chapter, we will cover the basic terms related to the issue of NCD IPO which will facilitate the understanding of NCD IPO.

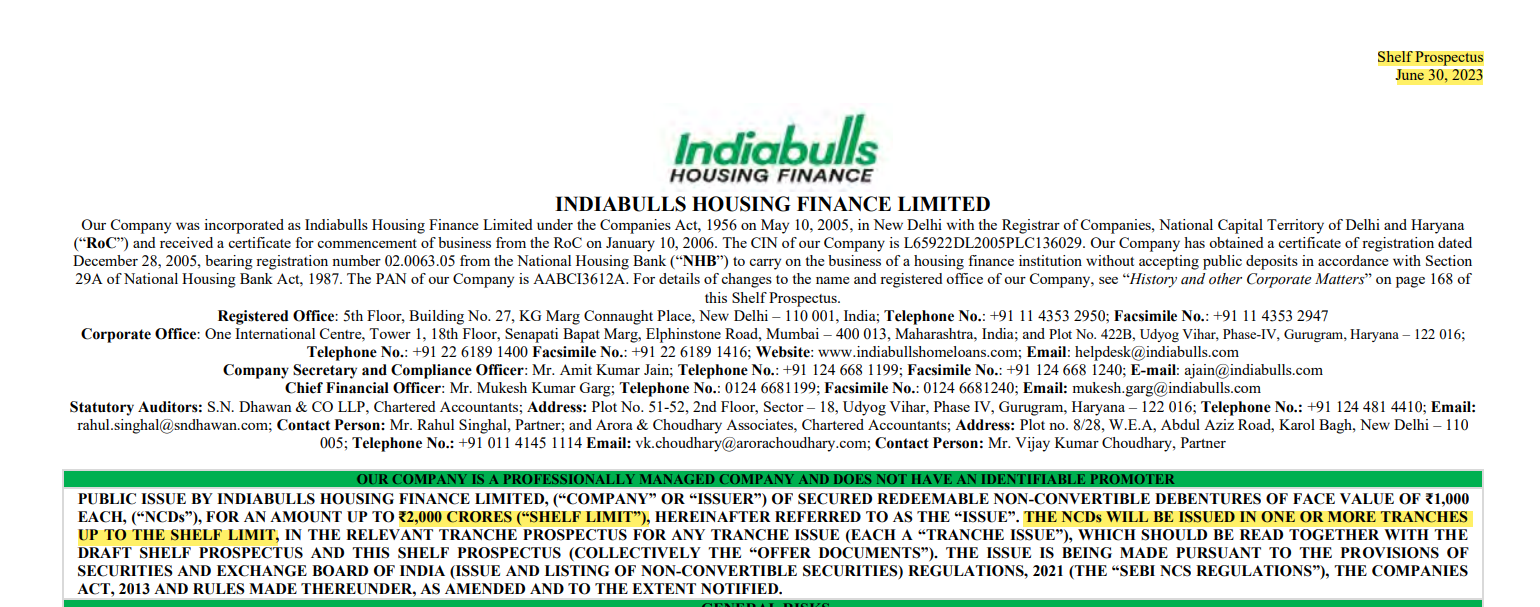

A shelf prospectus is the offering document that a company files with the regulator to register NCDs that it intends to offer over a specified period of time without having to file a separate prospectus for each offering. A shelf prospectus is usually valid for one year.

The shelf prospectus contains all the necessary information to help investors make an informed decision about their investment. A company must submit a draft and a final shelf prospectus with the regulator.

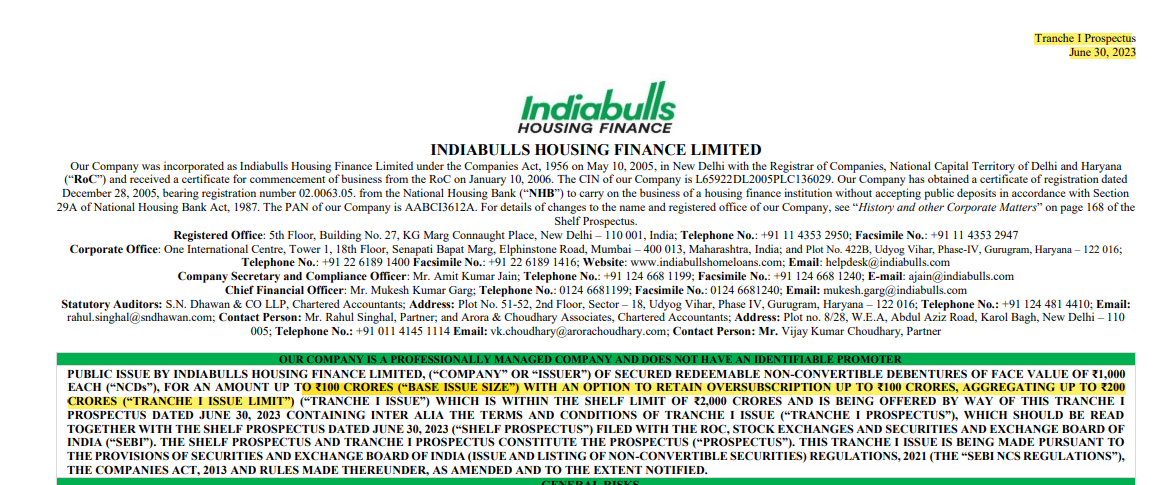

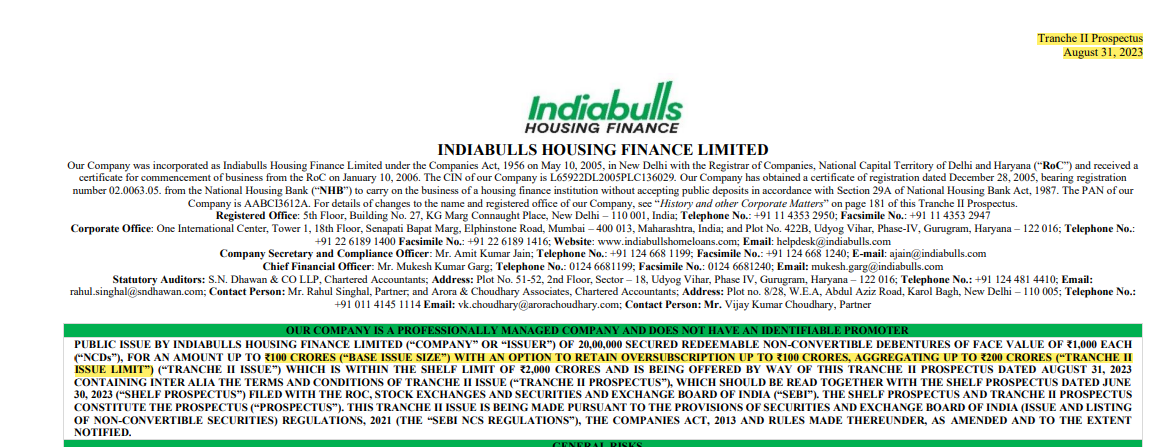

The Tranche Prospectus is the offering document issued for each NCD issue and contains the details of the issue and any material changes contained in the shelf prospectus or earlier Tranche Prospectus. The Tranche Prospectus is a subset of the Shelf Prospectus and must be read in conjunction with the Shelf Prospectus.

Shelf limit is the maximum size of an NCD issue. The company can raise funds in one or more tranches up to the shelf limit.

The base issue size is the minimum size of an NCD issue.

The issuing company may retain an oversubscription of up to 100% of the base issue volume. The retention of the oversubscription limit is subject to the credit rating and approval of the company's Management Board. This option to retain oversubscription also known as the "green shoe" option, allows the issuing company to sell more NCDs than the minimum issue size to meet the demand.

The tranche issue limit is the issue size post considering the option to retain oversubscription. The total tranche issue limit for the different tranches should not exceed the shelf issue limit.

Let us have a look at the NCD issues by Indiabulls Housing Finance in 2023 to understand the above terms

In June 2023, the company filed a shelf prospectus to raise up to Rs. 2,000 crores. Thereafter, the company offered NCDs in tranches in June, August, September and December 2023. The following excerpts from the NCD prospectus show that,

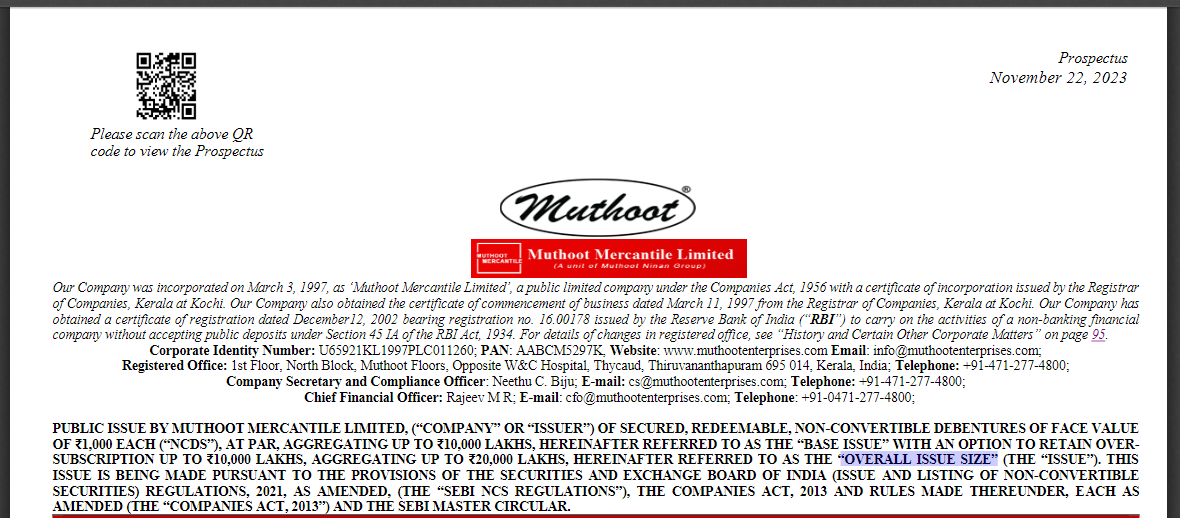

Generally, all companies planning an NCD issue file a shelf prospectus as companies raise funds through NCDs over a period of time and filing a fresh prospectus every time is a little tedious task. However, some companies choose to file a fresh offer document every time and some companies may not be eligible to issue a prospectus as per SEBI guidelines. (The criteria are discussed in a later chapter of the offer document).

In such cases, the company issues a draft prospectus and final prospectus just as done in the case of Equity IPO.

Overall Issue Size is the maximum size of the NCD issue. This term is used to refer to the issue size of NCDs when a company files a prospectus instead of a shelf prospectus.

The debenture redemption reserve, commonly referred to as DRR, is a fund maintained by the company for the payment of upcoming maturing debentures. Earlier, it was mandatory for all companies to maintain DRR as the company had to pay a penalty in case of non-compliance. The DRR was created from the funds earmarked for paying dividends or from a certain share of profits. The main purpose of the DRR was to reduce the likelihood that the company would be unable to meet its maturity obligations.

In accordance with the recent amendments to the Companies Act, 2013, and the Companies (Share Capital and Debentures) Rules 2014 and SEBI NCS Regulations, many companies are either exempted or have relaxations for the maintenance of DRR. The Company will provide the information on DRR requirements, if any, in the Prospectus.

The face value of the debenture is the original value of the debenture as mentioned on its certificate. It is the face value of the security, also known as the par value. The NCDs are issued at the face value. The NCD application amount is payable according to the face value and the number of debentures applied for.

NCD holder is the holder of the debenture in the company records. An NCD holder is not a shareholder of the company. Therefore, the rights of the NCD holder are limited and restricted to any changes or matters relating to the NCD.

The coupon rate is the rate of interest that is paid by the company on the NCD securities.

An NCD issue offers investors various options to choose the frequency of interest payments. An investor can choose to receive interest either monthly, annually or cumulatively.

The effective yield is the total return that an investor receives when his investment matures. The effective yield in case of cumulative interest payment option is always greater than the monthly or yearly interest payment option, as the interest amount is reinvested at the same rate until maturity.

The redemption date is the date on which the debt security must be repaid. It is the maturity date on which the investor receives his investment amount back with interest in accordance with the option chosen by the investor.

The redemption amount is the amount to be paid by the company to the investor in accordance with the selected plan. If the investor has chosen a cumulative plan, the entire investment amount together with the interest for the corresponding period will be paid by the Company as the redemption amount. In the case of monthly or annual interest payment plans, the investor only receives the principal amount and the interest for the coming month or year as a repayment amount.

Incentive is an additional rate of interest offered for certain categories of investors applying for NCD. Generally, this incentive is offered to HNIs and resident individuals provided they are :

AND/OR

The details of the investor category and the interest incentive are mentioned in the offer document.

Certain NCDs have a call and a pull option. In a call option NCD, the issuing company can call the NCD before maturity, i.e. it can buy back/repay the NCD before the redemption date, whereas in the put option, the NCD holder has the right to redeem the NCD before the maturity date. The Call Option and the Put Option may be exercised after the completion of a specified term of the NCD as mentioned in the Offer Document. If the Company has issued an NCD without Call Option and Put Option, the same will be specified as NA (not available) in the Offer Document.

An NCD with a call option usually has a higher interest rate than an NCD with a put option because an NCD with a call option is in favor of the issuing company, which has the right to buy it back at any time after a certain period of time.

The days count convention is the number of days for calculating interest. Interest calculations are performed for the actual days the NCD is held/invested.

Points to note:

Example:

An NCD is offering 9.25% interest for a tenor of 24 months with monthly, annually and cumulative interest payment options. Let us see how the number of days are calculated for payment.

Assumption: NCD got allotted on 27th July 2023 (Thursday)

NCD Day Count Convention Example

|

Interest Payment Option |

Instance |

Due Date |

Payment Date |

No. of days |

Interest |

|---|---|---|---|---|---|

|

Monthly |

1st Coupon |

27th August 2023 (Sunday) |

28th August 2023 (Monday) |

31 |

7.54 |

|

2nd Coupon |

27th September 2023 (Wednesday) |

27th September 2023 (Wednesday) |

31 |

7.54 |

|

|

3rd Coupon |

27th October 2023 (Friday) |

27th October 2023 (Friday) |

30 |

7.30 |

|

|

4th Coupon |

27th November 2023 (Friday) |

27th November 2023 (Friday) |

31 |

7.54 |

|

|

Similarly the no. of days from 5th Coupon to 23rd Coupon are calculated |

|||||

|

24th Coupon |

27th July 2025 (Sunday) |

25th July 2025 (Friday) |

30 |

7.30 |

|

|

Principal Amount |

27th July 2025 (Sunday) |

25th July 2025 (Friday) |

- |

1,000 |

|

|

Annually |

1st Coupon |

27th July 2024 (Saturday) |

29th July 2024 (Monday) |

366 |

92.5 |

|

2nd Coupon |

27th July 2025 (Sunday) |

25th July 2025 (Friday) |

365 |

92.5 |

|

|

Principal Amount |

27th July 2025 (Sunday) |

25th July 2025 (Friday) |

- |

1,000 |

|

|

Cumulative |

Interest Amount |

27th July 2025 (Sunday) |

25th July 2025 (Friday) |

731 |

193.85 |

|

Principal Amount |

27th July 2025 (Sunday) |

25th July 2025 (Friday) |

- |

1,000 |

|

The above table shows that if the interest payment date falls on a Saturday or Sunday, the interest is paid on Monday, i.e. the next working day. If the maturity date falls on a non-working day such as Saturday or Sunday, the maturity proceeds and any interest are paid on the previous working day, in this case Friday.

Green shoe option in NCD is the option to retain the excess subscription over and above the issue size.

A company can retain up to 100% of the minimum issue size. For example, if a company intends to raise Rs 200 crores , the green shoe option cannot exceed Rs 200 crores i.e. 100% of the basic issue size.

Debenture redemption reserve is a reserve created by the company to minimize the risk of default in payment of debenture amounts.

Debenture redemption reserve commonly known as DRR is created out of company profits that are earmarked to pay dividends. Earlier it was mandatory for all companies issuing NCD to maintain DRR failing which they were liable to pay penalty. However, in August 2019, the Ministry of Corporate Affairs (MCA) introduced certain relaxations in reference to maintenance of DRR.

No, as of August 2019, it is no longer mandatory for all companies to set up a debt redemption reserve (DRR).

Previously, it was mandatory for every company issuing NCDs to set up a DRR. In 2019, the MCA specified certain relaxations and exempted certain companies from maintaining DRR.

The prospectus of a company shall contain full details of DRR requirements.

The coupon is the interest rate that an NCD holder receives on the amount invested.

A company issuing NCDs offers a range of coupon rates for different maturities tenors with the option to receive coupon payments at different intervals such as monthly, annually or cumulative.

Every NCD has a maturity date.

NCDs are long-term fixed income investment instruments that mature after a period of more than 1 year to 20 years. NCDs cannot be withdrawn before maturity unless an NCD is listed or has a call or put option attached.

Listed NCDs can be traded like shares on the stock exchange. If an NCD holder wishes to exit the NCD early, he/she can sell it on the secondary market. If an NCD has a call or put option, either the company buys back the NCD before maturity or the NCD holder can redeem the NCD before maturity.

The redemption premium is the positive difference between the face value of the NCD and the redemption value of the NCD.

If the redemption amount of the NCD is greater than the face value of the NCD, this is referred to as a premium. In general, the debentures are issued at face value and repaid at a premium, taking into account the interest amounts.

Call option in NCD gives flexibility to the issuing company to withdraw from NCD before the maturity date.

In the call option, the issuing company can ask the NCD holder to surrender their NCD and take their investment amount back along with the interest due till then. An NCD with call option attached to it has a little higher rate of interest compared to NCDs with put option or normal NCD as it is in favour of the company.

Generally, a company exercises a call option in 2 scenarios:

A call option can only be exercised by the company after a certain period of the NCD has matured. A date for the exercise of the Call Option is specified in the Offer Document if the Call Option is applicable.

The full form of NCD IPO is Non-Convertible Debentures (NCDs) issued through Initial Public Offer. All non-convertible debentures that are listed on the stock exchange are called NCD IPOs.

Add a public comment...

FREE Intraday Trading (Eq, F&O)

Flat ₹20 Per Trade in F&O

|

|